Third Quarter 2025 Market Update

Third Quarter 2025 Market Update

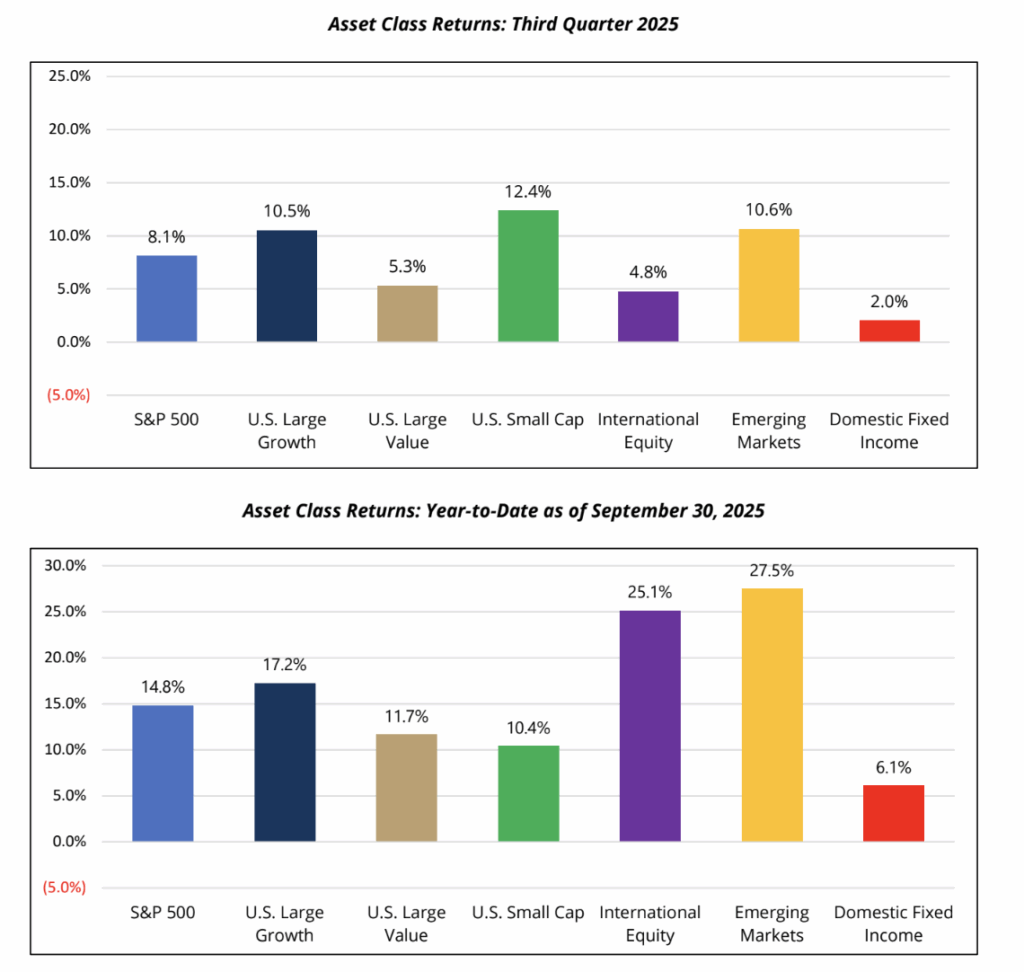

The third quarter of 2025 delivered strong returns across global equity and fixed income markets with the MSCI All Country World Index returning +7.6% (+18.4% YTD) and the Bloomberg U.S. Aggregate Bond Index gaining +2.0% (+6.1% YTD). In September, the U.S. Federal Reserve (“Fed”) resumed its easing cycle following a nine-month pause with an announced rate cut of 0.25%, bringing the benchmark for short-term interest rates to a range of 4.0% to 4.25%. The Fed’s first rate cut of the year provided a tailwind for both equity and fixed income markets, despite concerns of a softening U.S. labor market.

In equity markets, gains were broad-based across geographies, market capitalizations, and styles. The S&P 500 Index returned +8.1% (+14.8% YTD), fueled by resilient corporate earnings and continued investor enthusiasm for artificial intelligence (“AI”). After underperforming in the first half of the year, U.S. small-cap equities, as measured by Russell 2000 Index, rallied +12.4% during the quarter, bringing year-to-date performance +10.4%. From a sector perspective, information technology (+13.2% Q3, +22.3% YTD) and communication services (+12.0% Q3, +24.5%) outperformed, driven predominantly by AI themes. Defensive oriented sectors, including consumer staples (-2.4% Q3, +3.9% YTD) and healthcare (+3.8% Q3, +2.6% YTD) underperformed. Mixed economic data and continued inflationary pressures, particularly for lower-end consumers, have served as a headwind for certain consumer-oriented companies, while ongoing regulatory uncertainty has dampened returns in the healthcare sector.

Developed international equities, as measured by the MSCI EAFE Index, gained +4.8% for the quarter, bringing year-to-date performance to +25.1%. The MSCI Emerging Markets Index also outperformed during the period, returning +10.6% (+27.5% YTD). International equities have outperformed their U.S. counterparts thus far in 2025, driven by a weakening U.S. dollar, supportive fiscal spending initiatives in both Europe and Asia, and discounted relative valuations that have attracted increased investor flows. European members of the North Atlantic Treaty Organization (“NATO”) have committed to an estimated €800 billion on military defense initiatives by 2029. The increased spending, in response to pressures from the U.S. administration and geopolitical conflicts in Russia and Ukraine, has driven outsized returns for several European companies that stand to benefit.

Fixed income markets were positive for the quarter as yields moved lower following the Fed’s decision to cut rates. The Bloomberg U.S. Aggregate Bond Index returned +2.0%, bringing year-to-date performance to +6.1%. The 10-year and 2-year U.S. Treasury yields declined 22 and 30 basis points, respectively, finishing the period at 4.2% and 3.6%. Credit spreads also tightened during the period, supported by favorable investor sentiment and demand. The Bloomberg US Investment Grade and High Yield Corporate Credit indices returned +2.6% and +2.5%, respectively, for the quarter, bringing year-to-date performance to +6.9% and +7.2%. Municipal Bonds were also positive for the quarter with the Bloomberg Municipal Bond Index up +3.0% (+2.6% YTD).

In commodity markets, the Bloomberg Commodities Index returned +3.7% for the quarter (+9.4% YTD), led by gold and other precious metals. Gold prices hit new all-time highs, reaching approximately $3,833 per ounce at the end of the period. Gold has gained +44.8% for the year and has been a beneficiary of increased investor attention as an alternative to the U.S. dollar, a safe haven among trade uncertainty, and protection against concerns of the growing U.S. fiscal deficit.. Despite the escalation of conflicts in Russia/Ukraine and the Middle East during the quarter, oil markets were weaker primarily due to supply-side pressures. West Texas Intermediate Oil declined approximately 5% during the period, ending the quarter at $62 per barrel.

AI Driven Market & Looking Ahead

After a turbulent April triggered by tariff announcements and subsequent economic and geopolitical uncertainty, equity markets have staged a powerful recovery. While markets have generally shrugged off tariff-related risks for the time being, investors have fully embraced expectations for monetary easing from the Fed and resilient corporate earnings. AI has remained at the forefront of investor enthusiasm, which continues to be the dominant driver of market performance. This includes companies levered to AI-related infrastructure spending, spanning semiconductors, data centers, and power systems. Mega-cap technology companies have led the charge, buoyed by projections that global capital expenditures could scale to $3-4 trillion annually by 2030. A meaningful amount of the spending comes from “hyperscalers”, cloud service providers that offer large scale computing, data storage, and networking services that are essential to AI. These providers include Amazon (Amazon Web Services), Microsoft (Azure), Alphabet (Google Cloud), as well as Meta which uses these cloud services to run their own AI applications across its social media platforms. Collectively, these companies alone have committed greater than $350 billion to AI initiatives in 2025. AI themes have not only dominated equity market performance in 2025, but have also been a major contributor to economic growth. According to Rosenberg Research, AI spending accounted for nearly 100% of U.S. GDP growth in the first half of 2025. Investors believe the mega-cap hyperscalers have strong enough balance sheets and ample free cash flow to fund the announced AI investments. However, questions linger about financing sustainability should the massive level of investments fail to meet the aspirational AI efficiency gains and/or the applications cannot be commercialized to generate profits. Investment managers utilized by Prairie Capital maintain balanced views, which is generally supportive of the companies levered to the build out of AI infrastructure, while acknowledging there is undoubtedly some froth in valuations. Regardless of the view, the share price returns of companies tied to AI themes have meaningfully outperformed the overall market in 2025.

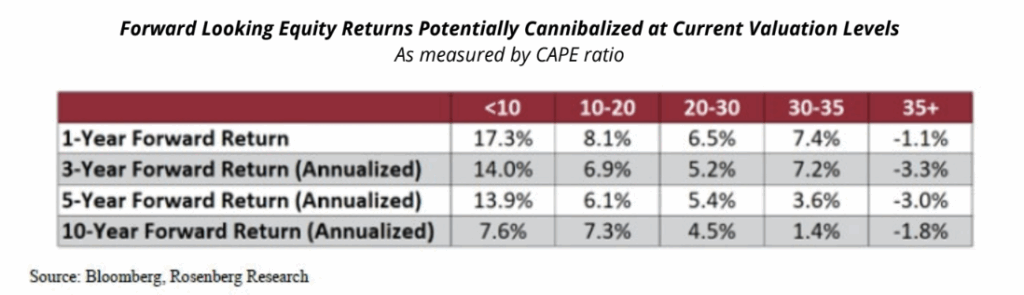

The outperformance of mega-cap technology companies has also driven the continued concentration of the top companies in the S&P 500 Index. At quarter-end, the top ten companies in the index represented 40.4% of the index, an all-time high. Concerns related to elevated U.S. equity markets valuations remain, as the S&P 500 Index ended the quarter trading at a 22.8x forward price-to-earnings (“P/E”) ratio, well above its 30-year average of 17x. The cyclically adjusted P/E ratio (“CAPE”) also ended the period trading at 37.5x, near its historical high. The denominator in the calculation of the CAPE ratio is the average inflation-adjusted earnings over the past 10 years. This calculation helps account for business cycles and seeks to provide a more stable comparison of valuations across different economic conditions. The elevated valuation metrics signal potentially compressed forward-looking returns for U.S. large-cap equity indices. While past performance is not indicative of future performance, forward returns over various time periods with a CAPE ratio greater than 35x have historically been negative, as noted in the table below.

Following the strong performance for risk assets during the quarter, we remain cautiously optimistic for the remainder of the year. With valuations for U.S. equity and fixed income markets near historical highs, we anticipate market volatility will remain elevated. Any real and/or perceived cracks in major themes across AI spending will likely create volatility, as well as headlines surrounding the Fed’s timing and magnitude of additional interest rate cuts. While the Fed decided to cut interest rates an additional 0.25 percentage points in October, there is a degree of uncertainty if the Fed will continue its easing path in December, given upside risks to inflation. On a related note, the collective impact of tariffs could start to show negative signs in the fourth quarter. The effective U.S. import tax climbed to approximately 17% as of September 30th, the highest level since the 1930s, and there are concerns that companies have largely exhausted easy tariff defenses, including pre-buying inventory or shifting sourcing to lower-tariff countries. Risks to inflation from tariffs remain, although shifts in the U.S. administration’s policies with global trading partners remains fluid.

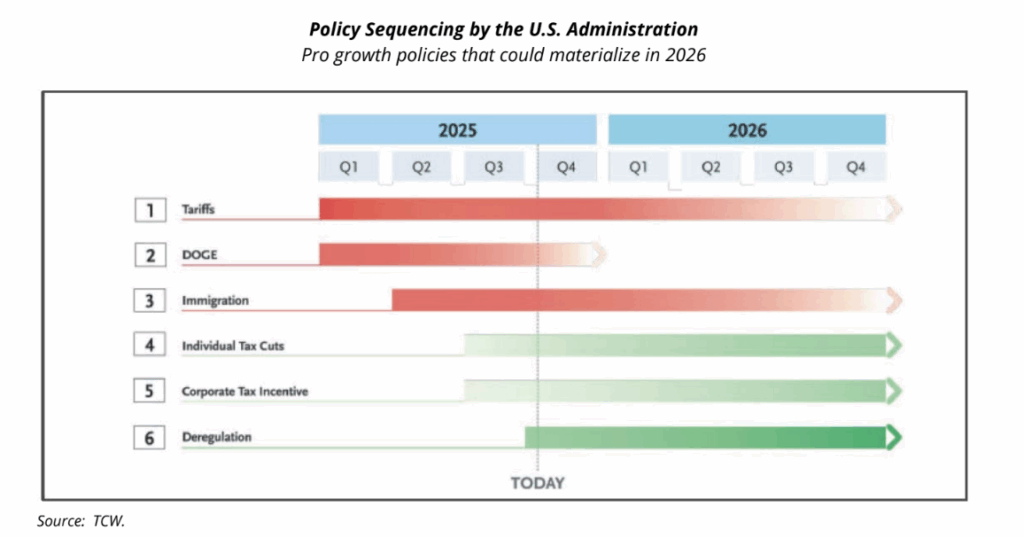

Looking ahead, while the U.S. administration has focused mostly on policy goals in 2025 that could potentially have a negative impact on growth, including tariffs, other policy goals with anticipated positive impacts could materialize in 2026. The passing of the One Big Beautiful Bill Act (OBBA) in July includes the extension of lower individual tax rates and introduces new tax deductions for individuals and corporations, including corporate tax incentives for research and development. The administration has also signaled deregulation goals that are expected to increase bank balance sheet capacity, infrastructure spending, and create a favorable environment for mergers and acquisitions that could be favorable for economic growth.

As always, we continue to advocate for diversification across portfolios, positioning for a range of potential outcomes while maintaining a steady focus on long-term objectives. A well-defined long-term plan, coupled with prudent risk management and close collaboration with your advisory team, provides the strongest foundation for ensuring your portfolio is well-positioned to meet your goals, especially during challenging market conditions. We remain committed to helping clients navigate turbulence in markets and are available to discuss your specific circumstances. As always, we appreciate the trust and confidence that you have placed in Prairie Capital.

Sincerely,

Prairie Capital Management Group, LLC

Important Disclosures

Past performance is not an indication of future results. This publication does not constitute, and should not be construed to constitute, an offer to sell, or a solicitation of any offer to buy, any particular security, strategy, or investment product. This publication does not consider your particular investment objectives, financial situation, or needs, should not be construed as legal, tax, financial or other advice, and is not to be relied upon in making an investment or other decision.

Certain information contained herein has been obtained or derived from unaffiliated third-party sources and, while Prairie Capital Management Group, LLC (“Prairie Capital”) believes this information to be reliable, makes no representation or warranty, express or implied, as to the accuracy, timeliness, sequence, adequacy, or completeness of the information. The information contained herein, and the opinions expressed herein, are those of Prairie Capital as of the date of writing, are subject to change due to market conditions and without notice and have not been approved or verified by the United States Securities and Exchange Commission (the “SEC”), the Financial Industry Regulatory Authority (“FINRA”), or by any state securities authority. This publication is not intended for redistribution or public use without Prairie Capital’s express written consent.

Definition: “YTD” = Year-to-Date.

Related Learning

February 17, 2026